Individual Health Insurance

- Voluntary Health Insurance Scheme

- Three Voluntary Health Insurance Scheme (VHIS) compliant plan options that provide the flexibility to select the medical coverage that best suits your needs.

- Cigna VHIS Series Overview

- Flexi Plan (Superior)

- Flexi Plan (SMM)

- Standard Plan

- High-End Medical Plan

- 360-degree global health protection that covers every key stage of your health and wellness journey.

- Cigna HealthFirst Elite 360 Medical Plan

- International High-End Health Plans

- Cigna Platinum Plan

- Cigna Cathay Premier Health Plan

- Term Critical Illness Plan

- Comprehensive protection for life’s unexpected health challenges, with flexible coverage options tailored to your needs.

- Cigna Healthcare VitalGuard Critical Illness PlanTM

- Medical and Health Series

- Cigna DIY Health Plan

- Cigna HealthFirst Choice Medical Plan

- Cigna Plus Medical Plan

- Cigna Civil Servants Medical Insurance Scheme

Group Health Insurance

- Global Health Benefits (For Employee)

- The most comprehensive, globally integrated health solutions tailored to meet diverse healthcare needs of your employees.

- Cigna Prime

- Healthcare Insights

- Read our latest research and studies on health and wellness

- Know more

- Your Health Plan, Your Growth Plan

- Learn how we can help your organization thrive

- Know more

Healthcare 360

- Medical Value-added Service

- Adding value to your health plan to support every step of your healthcare journey.

- Cashless Medical Service

- Day Procedure Centre Cashless Service

- Network List - Day Procedure Centres

- Cigna Care Manager Service

- Discover your Movement Age

- We partnered with FLEXR Technologies Ltd to create Flex-ray, a tool to analyse your Movement Health across four functional areas.

- Start Now

About Us

- About Us

- Learn about our commitment in improving the health and vitality of those we serve in Hong Kong since 1933.

- Cigna Healthcare Hong Kong

- Newsroom

- Receive updates on Cigna Healthcare Hong Kong

- Latest Updates

- Press Release

- Media Coverage

- Other Activities

- Careers

- Join our dedicated and dynamic team today

- Know more

Customer Service

- Medical Value-added Service

- Cashless Medical Service

- Day Procedure Centre Cashless Service

- Network List: Day Procedure Centres

- Cigna Care Manager Service

- Useful Information

- Useful Forms

- Payment Method

- Levy

- FAQ

- Contact Us

Individual Health Insurance

-

Voluntary Health Insurance Scheme

-

High-End Medical Plan

-

International High-End Health Plans

-

Term Critical Illness Plan

-

Medical and Health Series

Group Health Insurance

-

Global Health Benefits (For Employee)

-

Healthcare Insights

-

Your Health Plan, Your Growth Plan

Healthcare 360

-

Medical Value-added Service

-

Discover your Movement Age

-

Cigna Care Manager Service

-

Cigna Virtual Health Service

-

Smart Health

-

Health Insurance Basics

About Cigna Healthcare

-

About Us

-

Newsroom

-

Careers

Customer Service

-

Medical Value-added Service

-

Claims

-

Useful Information

Login

-

Individuals

-

Group Plan

-

Brokers

Cigna Healthcare VitalGuard Critical Illness PlanTM

Cigna Healthcare VitalGuard Critical Illness PlanTM

Empowering Recovery: Your Protector Against Health and Financial Burdens

Enjoy 35% premium discount and a complimentary mental wellness service for the first year upon successful enrolment. (Detail)

Get in Touch

By submitting this form, I understand the provision of above information means I agree to Cigna Healthcare's use and/or transfer of my personal data for direct marketing of its related insurance products and services. I have read and accepted the Personal Information Collection Statement of Cigna Healthcare.

Thank You for Choosing Cigna Healthcare

Our Cigna Customer Advisor will contact you soon

SORRY ABOUT THIS...

We are having trouble with your request. Please try again later

or Call (852) 8100 3705

Comprehensive Protection Tailored for Real Life

Up to HK$4,000,0001 Sum Insured

5-Year Critical Illness Coverage

– Guaranteed Renewal up to Age 85

Worldwide Second Medical Opinion

Service3

58 Critical Illnesses

4 Early Stage Critical Illnesses

+

43 Types of Surgeries

5 Juvenile Critical Illnesses

Flexible Coverage at Your Choice

Choose Sum Insured from HKD300K to HKD4M and receive 100% of the Sum Insured upon diagnosis of any of the 58 covered critical illnesses, including Cancer, Stroke, Heart Attack, and organ failure. (Details)

Early Stage Critical Illness Benefit

This benefit provides 20% of the Sum Insured for each diagnosis of early stage conditions, including Carcinoma-in-situ (claimable up to 2 times in different organs), Early Stage Cancer, Surgery Coverage, and Juvenile Critical Illnesses.

Surgery Coverage

Major procedures shouldn’t create major financial stress. Our plan includes 20% of the Sum Insured for covered surgeries across multiple body systems—counted under the early stage critical illness benefit.

For full coverage details, including all listed illnesses, claim limits, exclusions and relevant rules, please refer to the product brochure here.

Remarks:

- Sum Insured is subject to the insured’s age range and the Sum Insured selected at enrollment.

- Premium is level for 5 years and the premium level is subject to change from time to time due to medical inflation and overall market claims experience.

- This service is a value-added service provided by an independent third-party service provider and does not form part of the contractual benefit under your policy. Cigna Healthcare reserves the right to amend or cancel the service at any time without prior notice at its absolute discretion. Cigna Healthcare is not the service provider for this service. The relevant service provider is not our agent, and vice versa. We make no representation, warranty or undertaking as to the quality and availability of the service, and do not accept any responsibility or liability for the service provided by the service provider. Under no circumstances will Cigna Healthcare be responsible or liable for acts or omissions of the service provider in the provision of the service.

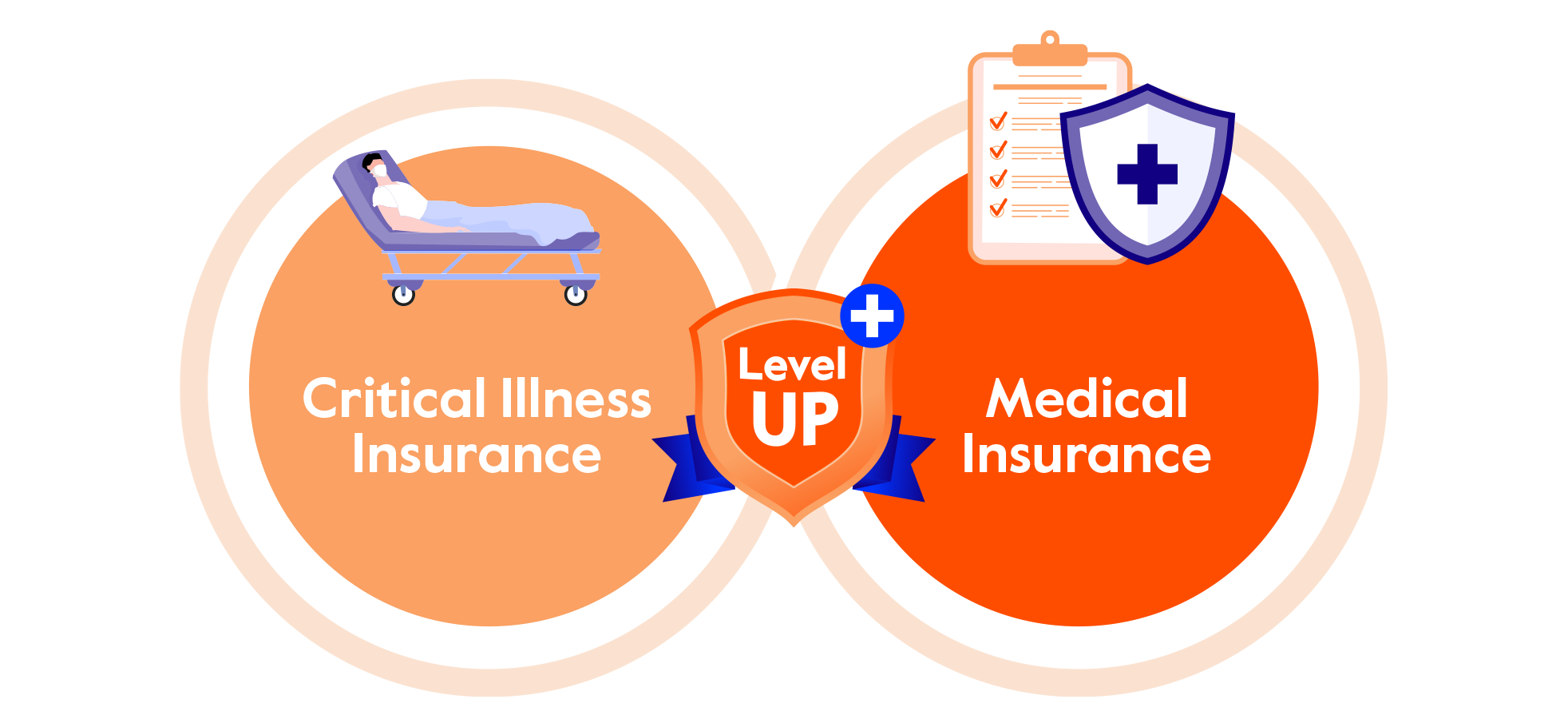

Your Ideal Protection Combo

If you are currently covered by a medical insurance plan, you can enhance your protection by adding critical illness coverage. This provides support for unexpected health challenges, from treatment costs to daily living expenses, offering more comprehensive protection for you and your loved ones.

We offer term critical illness plan that are easy to get started with and designed to help you handle sudden health issues with confidence.

Whether facing a sudden diagnosis or navigating a long-term recovery, Critical Illness Insurance and Medical Insurance serve distinct yet complementary roles. Check our FAQ to learn more about the benefits of double protection.

Value-added Service

Worldwide Second Medical Opinion Service1,2

Access to an independent second opinion from global renowned medical centres on your diagnosis and treatment plan, empowering you to make an informed decision about the best treatment options.

Remarks:

- This service is a value-added service provided by an independent third-party service provider and does not form part of the contractual benefit under your policy. Cigna Healthcare reserves the right to amend or cancel the service at any time without prior notice at its absolute discretion. Cigna Healthcare is not the service provider for this service. The relevant service provider is not our agent, and vice versa. We make no representation, warranty or undertaking as to the quality and availability of the service, and do not accept any responsibility or liability for the service provided by the service provider. Under no circumstances will Cigna Healthcare be responsible or liable for acts or omissions of the service provider in the provision of the service.

- The “Worldwide Second Medical Opinion Service” is an independent opinion provided by the global medical centre and does not represent Cigna Healthcare’s clinical stance. It is intended to supplement the information the Insured Person has already received from his/her attending doctor and should not be used to substitute the attending doctor’s recommendations.

Plan Details

| Plan Name | Cigna Healthcare VitalGuard Critical Illness PlanTM |

|---|---|

| Product Brochure | |

| Product Type | Basic plan |

| Premium Structure | 5-year Term1 |

| Premium payment frequency | Annually / Monthly |

| Entry Age (at last birthday) |

15 days to Age 65 |

| Benefit Term | 5 year term, guaranteed renewal up to age 85 of the Insured | ||||||||||

| Policy currency | HKD | ||||||||||

| Sum Insured | Minimum amount: HKD300,000

|

||||||||||

| Critical Illness Benefit2 | 100% of Sum Insured (Less any Early Stage Critical Illness Benefit paid or payable; Less any indebtedness) |

||||||||||

| Early Stage Critical Illness Benefit2 | Advances 20% of Sum Insured3 (Less any indebtedness) |

- Premium is level but non-guaranteed and may be adjusted at each policy anniversary.

- For full details of the Benefit coverage and Sum Insured, please refer to the Benefit Schedule.

- The aggregate amount of all benefits paid and payable in respect of each claim of Early Stage Critical Illness Benefit under all critical illness policies issued by the Company shall not exceed HKD400,000. For each claim, the payable amount will be limited to the lesser of (i) 20% of the Sum Insured or (ii) HK$400,000 less the total amount of benefits paid and/or payable in respect of the same Early Stage Critical Illness under all other policies of Cigna Healthcare VitalGuard Critical Illness PlanTM for the same Insured Person issued by the Company.

Case Illustration

The examples are hypothetical and for illustrative purposes only and assume that- all premiums are paid in full when due, and

- underwriting requirements and claims requirements of the benefits are fulfilled.

| Policy Holder and Insured Person | Rex |

| Age | 38 (non-smoker) |

| Background | At 38, Rex was at the peak of his career, focused on building a stable and fulfilling life. As a young professional, he understood that health risks could arise unexpectedly. To protect himself from the financial impact of serious illness, he chose to enroll in Cigna Healthcare VitalGuard Critical Illness PlanTM. |

| Sum Insured | HK$1,500,000 |

| Annual Premium at Policy Inception | HK$7,860* |

Total Financial Support: HK$1,500,000

Total Premium Paid*: HK$31,440

Over the years, Rex received a total of HK$1,500,000 (100% payout of the Sum Insured).

This financial support:

- Finical security for the loss of income during his recovery

- Cover medical bills, rent, and daily living expenses

- Ease the burden on his family, allowing him to focus on healing

- Maintain his quality of life even while unable to work

Why It Matters

For young professionals like Rex, Cigna Healthcare VitalGuard Critical Illness PlanTM offers flexible and comprehensive coverage. When health challenges arise, it provides immediate financial support so he can focus on recovery, not expenses.

Remark:

*Premium is level for 5 years and the premium level is subject to change from time to time.

First Claim (Age 41)

100% of the Sum Insured: HK$1,500,000

The Unexpected Diagnosis: Lung Cancer

Three years into his policy, Rex began experiencing unusual symptoms. After medical evaluation, he was diagnosed with Lung Cancer, one of the 58 covered critical illnesses under the plan. The news was devastating for him and his family.

Rex required surgery and chemotherapy, and was unable to work for 18 months. Beyond the physical toll, he faced immense emotional stress and was afraid to rely on him and his family’s savings to cover daily expenses.

| Policy Holder and Insured Person | Stella |

| Age | 35 (non-smoker) |

| Background | Stella is a 35-year-old wife and mother to a 7-year-old daughter and a 6 year-old son. As the caregivers, she works hard to provide stability and build a secure future. Despite a tight budget, she understands the importance of protection, so she enrolled in Cigna Healthcare VitalGuard Critical Illness PlanTM, ensuring her and her family has financial support if the unexpected happens. |

| Sum Insured | HK$1,000,000 |

| Annual Premium at Policy Inception | HK$4,780* |

Total Financial Support: HK$1,000,000

Total Premium Paid*: HK$23,900

Over the years, Stella received a total of HK$1,000,000 (100% payout of the Sum Insured):

- HK$600,000 from three early stage critical illness claims

- HK$400,000 from the critical illness claim

This financial support:

- Covered lost income and fixed expenses

- Maintained her family’s lifestyle

- Focus on recovery without added financial stress

Why It Matters

For young families like Stella's, Cigna Healthcare VitalGuard Critical Illness PlanTM provides practical, flexible, and comprehensive protection. It ensures financial stability during health crises, allowing her and her family to focus on recovery and peace of mind.

Remark:

*Premium is level for 5 years and the premium level is subject to change from time to time.

First Claim (Age 36)

20% of the Sum Insured:HK$200,000

Two years after enrolling, Stella was diagnosed with Cervical Cancer (Carcinoma-in-situ). The diagnosis was unsettling, but her plan provided immediate financial support.

Second Claim (Age 37)

20% of the Sum Insured:HK$200,000

A year later, Stella underwent a Valve replacement surgery. The unexpected need for surgery deeply affected her, both physically and emotionally.

Third Claim (Age 38)

20% of the Sum Insured:HK$200,000

Soon after, Stella was diagnosed with Esophageal Cancer (Carcinoma-in-situ). While treatable, the repeated illnesses strained both her emotional and financial resilience.

Fourth Claim (Age 39)

HK$400,000

(100% - 60% advanced payment of the Sum Insured)

Three years later, Stella faced her toughest challenge yet: Colon Cancer

She required surgery and chemotherapy and was unable to work for 18 months, causing a significant loss of income. She also reached out to Worldwide Second Medical Opinion Service for independent second opinion on the treatment plan.

| Policy Holder and Insured Person | Ryan |

| Age | 29 (non-smoker) |

| Background | Ryan and Emma, both 29, had just entered a new chapter in life, newly married and proud owners of their first home. Their hearts were full of hope and excitement for the future. But with mortgage payments and rising living costs, financial planning has become a top priority. Ryan already had a basic medical insurance plan that covered hospitalization and medical costs. However, he understood that if a serious illness were to strike, medical insurance alone might not be enough to cover long-term recovery expenses or the impact of lost income. To strengthen their safety net, Ryan chose to enroll in Cigna Healthcare VitalGuard Critical Illness PlanTM. |

| Sum Insured | HK$1,000,000 |

| Annual Premium at Policy Inception | HK$2,800* |

Total Financial Support: HK$1,000,000

Total Premium Paid*: HK$5,600

Over the years, Ryan received a total of HK$1,000,000 (100% payout of the Sum Insured):

- HK$200,000from early stage critical illness claim

- HK$800,000 from the critical illness claim

This financial support:

- Financial stability during a difficult time

- Emotional reassurance and reduced stress

- Benefits of double protection —medical and financial

- The ability to maintain their lifestyle

Why It Matters

For young couples starting a life together, critical illness protection is not just an insurance plan; it is a promise for the future. Even with medical coverage in place, Cigna Healthcare VitalGuard Critical Illness PlanTM offers additional financial support when it is needed most, becoming a strong pillar of support during life’s unexpected health challenges.

Remark:

*Premium is level for 5 years and the premium level is subject to change from time to time.

First Claim (Age 29)

20% of the Sum Insured: HK$200,000

In the first year of his policy, Ryan was diagnosed with Thyroid Cancer (Carcinoma-in-situ), an early stage critical illness covered under the plan. He received an immediate payout which helped cover daily expenses and filled the gaps not covered by his medical insurance.

Second Claim (Age 30)

HK$800,000

(100% - 20% advanced payment of the Sum Insured)

A year later, Ryan was diagnosed with Heart Attack, one of the critical illnesses covered by the plan. Under the policy terms, he received the remaining sum insured. While his medical insurance covered hospitalization and medical costs, the critical illness payout from this plan gave Ryan and Emma the financial breathing room and they needed to focus on recovery without worrying about bills or mortgage payments.

Have questions?

We’re here to help! Call now for expert advice and personalized recommendations.

Application & Enquiry Hotline:

FAQ

About Product

Why should I purchase the Cigna Healthcare VitalGuard Critical Illness (CI) plan?

- CI serves as an income protection vehicle: designed to hedge against the unforeseen financial burden that may arise from being unable to work due to serious medical conditions.

- Medical expense safeguard: critical illness insurance is not a replacement for health insurance; it’s a supplement. It helps cover costs that traditional health plans do not, especially if you have a high-deductible plan or limited coverage.

Should I still purchase Critical Illness (CI) insurance if I already have medical insurance?

If you are currently covered by a medical insurance plan, you may consider enhancing your protection by adding critical illness coverage. Medical insurance typically reimburses hospital and treatment costs, while critical illness insurance provides a lump-sum payout upon diagnosis of a covered illness. This payout can be used flexibly for daily living expenses, mortgage payments, or income replacement, offering additional financial support during recovery. Critical illness coverage is designed to supplement your existing medical insurance, helping you manage unforeseen financial burdens that may arise from serious medical conditions.

| Critical Illness Insurance | Medical Insurance | |

|---|---|---|

| Coverage | Covers critical illnesses and early stage critical illnesses | Covers hospitalization, surgery, outpatient treatment, and other eligible medical expense |

| Benefit Type | Lump sum compensation to replace income and support daily living | Reimbursement of actual medical expenses incurred |

| Benefit usage | Flexible use for living expenses, recovery, or family needs to maintain quality of life | Covers eligible hospitalization and medical costs |

| Payout | Immediate lump sum compensation upon diagnosis | Reimbursements made after treatment, based on actual expenses or via Cashless Medical Service |

| Purpose | Provides financial support to help you and your family reduce economic stress, enabling you to focus on recovery | Provides comprehensive medical support across all stages of health journeys from prevention, diagnosis, treatment, to recovery. Eases treatment burden and includes rehabilitation, extended care benefits and value-added services |

What is the difference between Term Critical Illness insurance and Savings-linked Critical Illness insurance?

- Term Critical Illness Insurance: Pure protection plan with affordable premiums, offering coverage for a fixed term (e.g., 5 years) and guaranteed renewal up to certain age. It focuses on financial support during illness without any savings component.

- Savings-linked Critical Illness Insurance: Combines protection with a savings or investment element, generally with higher premiums and long-term commitment. It builds cash value over time but is less cost-effective for pure protection needs.

Does the plan have a cooling-off period?

*For full details and procedural requirements, please refer to the Important Information section on this website or brochure.

Is there any Waiting Period for the Cigna Healthcare Critical Illness (CI) plan?

90 Days from the Policy Issuance Date or the Policy Effective Date (whichever is the later).

Waiting Period shall mean a period of ninety (90) days from the latest of:

- the benefit issuance date or the benefit effective date (whichever is the later); or

- the issue date or the effective date of the increase in the Sum Insured (whichever is the later) or

- the effective date of reinstatement (if applicable).

Is there any Value-added service (VAS) for the Cigna Healthcare Critical Illness (CI) plan?

Will the premium remain unchanged for the Cigna Healthcare Critical Illness (CI) plan over the next 5 years?

How much Critical Illness Insurance coverage should I purchase?

It depends on your age, income, family obligations, and lifestyle. Our plan offers coverage from HK$300,000 up to HK$4,000,000, subject to age limits:

Age 18–45: up to HK$4,000,000

Age 46–55: up to HK$2,500,000

Age 56–65: up to HK$1,000,000

Consider factors like mortgage, children’s education, and living expenses to ensure sufficient protection against income loss and recovery costs.

Application

Can I purchase the Cigna Healthcare Critical Illness (CI) plan today and add more protection in future as multiple policies?

How to enroll in Cigna Healthcare VitalGuard Critical Illness PlanTM?

Claims

How to claim?

To make a claim to your policy, please download “MyCigna HK” app from the App Store or Google Play store and register user account to access it.

When submitting a claim through MyCigna HK, please have the documents below ready.

Below required documents must be received within 180 days after the date of the event or first diagnosis of the illness (Please refer to actual policy terms and conditions).

- Completed Critical Illness Claim Form (Part I)

Download the Critical Illness Claim Form - Attending Physician Statement completed by your attending doctor (Part II of the Claim Form)

- Hospital Discharge Summary or any document(s) issued by doctor / hospital with diagnosis proof (If applicable)

- Identity card copy of the Policyholder/Insured Person

- Copy of all histopathological reports (Applicable to cancer / early-stage malignancy)

- Copy of CT scan and MRI reports (Applicable to stroke)

- Copy of all reports such as ECG, exercise stress test, echocardiogram, enzymes assays, angiograms, coronary angiography reports etc. (Applicable to heart disease)

- Copy of all relevant laboratory test, imaging and diagnostic test reports (If applicable)

Your request will be processed immediately upon receipt of the form with complete information. Should you need further assistance, please feel free to contact either of following:

- Your Financial Consultant

- Cigna VitalGuard Customer Service Hotline: (852) 2233 4888 (Mon – Fri, 0900 - 1730, except Public Holidays).

How many claims can I have?

- Critical Illness Benefit*: Payable once at 100% of the Sum Insured, less any Early Stage Critical Illness Benefit paid and/or payable, and less Indebtedness (if any); policy terminates after payout.

- Early Stage Critical Illness Benefit*:

- The Early Stage Critical Illness Benefit can be claimed for each Early Stage Critical Illness once only. For each claim, the benefit amount is 20% of the Sum Insured or up to HK$400,000 (whichever is lesser).

- The Early Stage Critical Illness Benefit can be claimed in respect of Carcinoma-in-situ for up to 2 times, provided that the 2 claims must be in respect of Carcinoma-in-situ occurring in 2 different organ(s). For each claim, the benefit amount is 20% of the Sum Insured or up to HK$ 400,000 (whichever is lesser)

- The policy shall terminate and cease to provide any coverage when the aggregate amount of the Early Stage Critical Illness Benefit paid reaches 100% of the Sum Insured.

Termination

What should I do if I need to terminate my policy? What would happen to the premium paid for the policy year?

You may cancel your policy and obtain refund of the Standard Premium and Premium Loading (if any) and insurance levy paid within the cooling off period (the earlier of 30 days after the delivery of the policy or the cooling-off notice to you or your representative), you have to tell us by completing a form prescribed by us if you decide to cancel the policy.

After cooling off period, the Policy Holder may terminate the policy by giving not less than 30 days’ notice in writing to Cigna Healthcare in a form prescribed by us. Such termination shall become effective on the date specified in such form or the date approved by us, whichever is the later. There shall be no refund of the Standard Premium, the Premium Loading (if any) and insurance levy paid and Cigna Healthcare reserves the right to charge the Standard Premium and the Premium Loading (if any) calculated until the end of such Policy year which termination of this policy becomes effective.*

* For full details and exceptions, please refer to the Important Information section on this website or in the product brochure.Enquiry and Others

Any contact points for enquiry?

(Mon – Fri, 0900 - 1730, except Public Holidays).

Remarks:

The above information is for Hong Kong only and the above product is intended for sale in Hong Kong only. All information here is for reference only. The product information provided on this website is for general reference only and does not constitute the full terms and conditions of the policy. For detailed definitions of specified terms, specific coverage conditions, exclusions, and complete terms, please refer to the brochure and policy document. The above information should not be regarded as any form of offer or recommendation to purchase insurance. Please read and understand the product details before making a purchase.

Terms & Conditions

IMPORTANT INFORMATION

The product information provided on this website is for general reference only and does not constitute the full terms and conditions of the policy. For detailed definitions of specified terms, specific coverage conditions, exclusions, and complete terms, please refer to the policy document.

Cooling Off Right

You may exercise the right to cancel the policy and obtain a refund of the standard premium and premium loading (if any) and insurance levy paid within the cooling-off period.

The cooling-off period is the period of 30 days immediately following the day of the delivery of the policy or the cooling-off notice (whichever is the earlier), to you or your nominated representative. The cooling off notice is a notice that will be sent to you or your nominated representative by Cigna Worldwide General Insurance Company Limited to notify you of the cooling-off period around the time the policy is delivered.

To exercise this right, a written notice of cancellation must be signed by you or the request to cancel must be made by you in a form prescribed by the Company and received directly by the Company at 16/F, 348 Kwun Tong Road, Kwun Tong, Kowloon, Hong Kong. In such event, the policy shall be deemed to have been void from the policy effective date and the Company shall not be liable to pay any benefit.

No refund can be made if a benefit payment has been made, is to be made or pending.

Policy Cancellation

After the cooling-off period, you may cancel the policy by giving not less than 30 days notice to us using a form prescribed by the Company.

Termination of the policy caused by such cancellation shall become effective on the date specified in such form or the date approved by the Company, whichever is the later.

There shall be no refund of the standard premium, the premium loading (if any) and insurance levy paid. The Company reserves the right to charge the standard premium and the premium loading (if any) calculated until the end of such policy year during which the termination of the policy becomes effective.

Mis-statement of non-health related information

If any non-health related information (E.g. age, sex or smoking Habit) of the Insured Person has been mis-stated in the Application or in any subsequent information or document submitted to the Company for the purpose of the application, the Company may adjust the premium payable on the basis of the correct information or declare the Policy void as from the Policy Effective Date if the application of the Insured Person should have been rejected based on the correct information.

Misrepresentation or fraud

If any material fact relating to the health related information of the Insured Person has been incorrectly stated in, or omitted from the application or any statement or declaration made for or by the Insured Person in the application or in any subsequent information or document submitted to the Company for the purpose of the application; or any application or claim submitted is fraudulent or where a fraudulent representation is made, the Company may declare the policy void as from the policy effective date.

Premium

Premium payable

For the basic policy, you are required to pay the standard premium and the premium loading (if any) regularly on the premium due date.

Non-payment of premium

If you fail to pay the initial premium in full for the policy on or before the policy issuance date or the policy effective date (whichever is the earlier), the policy shall be deemed to be void as from the Policy Effective Date for all purposes. Accordingly, we shall not be liable to pay any benefit under the policy.

Except for the initial premium payment, a grace period after any premium due date will be allowed for payment of premium or any part thereof. The coverage of the policy will remain in force during this grace period, but the Company shall have the right to deduct at its discretion any due premium payment from the benefit payable under the policy if there is any benefit payable during the grace period.

If the standard premium and premium loading (if any) of the Basic Policy or any part thereof remains unpaid at the end of the grace period, the policy shall terminate on the premium due date on which the unpaid standard premium and premium loading (if any) was first due.

Premium Adjustment

The Company reserves the right to revise the standard premium of the Policy on each anniversary date at its sole discretion by taking into account such factors as the Company determines to be relevant for the purpose of revising the standard premium. If the premium loading is set as a percentage of the standard premium, the amount of premium loading will be adjusted automatically according to the change in the standard premium.

Claims Procedure

To make a claim, please download and register for the MyCigna HK app. For details of procedures by claims type, please visit the Company website https://www.cigna.com.hk/en/customer-service/insurance-claim-procedure.

A fully completed claim form prescribed by the Company must be given to the Company during the lifetime of the insured person and within 60 days (a) after the date of the event giving rise to the claim or (b) after the first diagnosis of critical illness or early stage critical illness (whichever is the earlier). Such form shall include information sufficient to identify the insured person and the nature of the claim.

Benefits

Coverage is subject to compliance with sanctions rules under policy provisions.

Critical Illness Benefit

Subject to the terms and conditions of the policy, while the policy is in force and after the Waiting Period, if the insured person is first diagnosed to be suffering from a critical illness, the Company shall pay the Critical Illness Benefit to the policy holder in 1 lump sum calculated in accordance with the formula as follows:

Critical Illness Benefit payable 100% of the Sum Insured

LESS ( - )

Any Early Stage Critical Illness Benefit paid or payable

LESS ( - )

Indebtedness (if any)For the avoidance of doubt, the policy shall terminate and cease to provide any coverage upon payment of the Critical Illness Benefit.

Early Stage Critical Illness Benefit

Subject to the terms and conditions of the policy, while the policy is in force and after the Waiting Period, if the insured person is first diagnosed to be suffering from an early stage critical illness, the Company shall pay the Early Stage Critical Illness Benefit to the Policy Holder calculated in accordance with the formula as follows:

Early Stage Critical Illness Benefit payable (for each Early Stage Critical Illness) The lesser of:

(a) 20% of the Sum Insured; or

(b) HK$400,000 less the total amount of benefits paid and/or payable in respect of the same Early Stage Critical Illness under all other policies of Cigna Healthcare VitalGuard Critical Illness PlanTM for the same Insured Person issued by the Company

LESS ( - )

Indebtedness (if any)The Early Stage Critical Illness Benefit can be claimed for each early stage critical illness once only under the Policy. Notwithstanding the aforementioned, the Early Stage Critical Illness Benefit can be claimed in respect of “Carcinoma-in-situ” for up to 2 times, provided that the 2 claims must be in respect of “Carcinoma-in-situ” occurring in 2 different organ(s). In this regard, once “Carcinoma-in-situ” is diagnosed in 1 covered organ, that organ is excluded for purposes of a second claim for “Carcinoma-in-situ” under the Early Stage Critical Illness Benefit. If the relevant organ has both a left and a right component (such as, but not limited to, the lungs or breasts), the left side and right side of the organ shall be considered as 1 and the same organ.If the Insured Person is insured under more than 1 policy of “Cigna Healthcare VitalGuard Critical Illness PlanTM” issued by the Company, the total amount of benefits paid and/or payable in respect of each and the same early stage critical illness under all such policies shall not exceed HK$400,000. Notwithstanding the aforementioned, if the Insured Person is insured under more than 1 policy of Cigna Healthcare VitalGuard Critical Illness PlanTM issued by the Company: (a) the total amount of benefits paid and/or payable in respect of each claim for “Carcinoma-in-situ” under all such policies shall not exceed HK$400,000; and (b) the total amount of benefits paid and/or payable in respect of the 2 claims for “Carcinoma-in-situ” under all such policies shall not exceed HK$800,000.

The Early Stage Critical Illness Benefit can be claimed multiple times and the aggregate amount of the Early Stage Critical Illness Benefit paid and/or payable under the Policy shall not exceed 100% of the Sum Insured.

For the avoidance of doubt, the policy shall terminate and cease to provide any coverage when the aggregate amount of the Early Stage Critical Illness Benefit paid reaches 100% of the Sum Insured.

Renewal

The basic policy shall be effective for the period of cover and thereafter guaranteed to be automatically renewable for each subsequent period of cover, provided that the standard premium and premium loading (if any) is paid on or before each premium due date and that we continue to issue new policy(ies) under the basic policy.

The Company reserves the right to revise the standard premium on each Anniversary Date at its sole discretion by taking into account such factors as the Company determines to be relevant for the purpose of revising the standard premium.

The Company reserves the right to revise the terms and conditions and/or the Benefit Schedule of the policy upon each renewal.

If the basic policy is not renewed by the Company, we will send a written notice to you, at least before 30 days prior to the next renewal date, to notify you that the policy will not be renewed.

Termination

The policy shall terminate upon the occurrence of the earliest of the following events:

(a) the death of the insured person;

(b) the policy is canceled during the cooling-off period;

(c) the cancellation of the policy by the Policy Holder;

(d) the cancellation of the Policy by the Company due to mis-statement of non-health information, misrepresentation or fraud, non-payment of initial payment;

(e) the policy is non-renewal that we discontinue to issue new policy(ies)

(f) the lapse of the policy following the non-payment premium by the end of the grace period;

(g) upon payment of the Critical Illness Benefit;

(h) when the aggregate amount of the Early Stage Critical Illness Benefit paid reaches 100% of the Sum Insured; or

(i) on the anniversary date immediately after the insured person reaches age 85.

Inflation Risk

Your current planned benefit may not be sufficient to meet your future needs since the future cost of living may become higher than they are today due to inflation. Where the actual rate of inflation is higher than expected, you may receive less in real terms even if the Company meet all of our contractual obligations.

Medically Necessary

"Medically Necessary" shall mean the need to have medical service for the purpose of investigating or treating the relevant disability in accordance with the generally accepted standards of medical practice and such medical service must:

(a) require the expertise of, or be referred by, a registered medical practitioner;

(b) be consistent with the diagnosis and necessary for the investigation and treatment of the disability;

(c) be rendered in accordance with standards of good and prudent medical practice, and not be rendered primarily for the convenience or the comfort of the insured person, his family, caretaker or the attending registered medical practitioner;

(d) be rendered in the setting that is most appropriate in the circumstances and in accordance with the generally accepted standards of medical practice for the medical services; and

(e) be furnished at the most appropriate level which can be safely and effectively provided to the insured person.

Waiting Period

“Waiting Period” shall mean a period of 90 days from the latest of:

(a) the policy issuance date or the policy effective date (whichever is the later); and

(b) the effective date of reinstatement (if the policy has been reinstated).

In respect of any increase in benefits resulting from a higher Sum Insured under the policy, "Waiting Period" shall mean a period of 90 days from the latest of:

(a) the issue date or the effective date of the increase in the Sum Insured (whichever is the later); and

(b) the effective date of reinstatement (if the policy has been reinstated).

Key Exclusions

The product information provided in this website is for general reference only and does not constitute the full terms and conditions of the policy. For detailed definitions of specified terms, specific coverage conditions, exclusions, and complete terms, please refer to the policy document.

Under the policy, the Company shall not pay any benefits in relation to or arising from the following:

(a) any disability other than a diagnosis of critical illness or early stage critical illness;

(b) any disability the signs or symptoms of which, or any surgery the cause or triggering condition of which, first occurred prior to the policy issuance date or the policy effective date (whichever is the later);

(c) any disability the signs or symptoms of which, or any surgery the cause or triggering condition of which, first occurred during the Waiting Period;

(d) Fulminant Viral Hepatitis or Cancer suffered by the insured person, where in our opinion such disease was directly or indirectly due to AIDS or HIV Infection (except for AIDS/HIV due to Blood Transfusion, Occupational Acquired HIV, HIV Infection due to Organ Transplant, and Medically Acquired HIV Infection);

(e) any disability or surgery caused by suicide, attempted suicide or intentionally self-inflicted injury, whether sane or insane;

(f) any disability or surgery directly or indirectly caused by the taking of drugs (except under the direction of a doctor), the consumption of poison or alcohol;

(g) any disability resulting from a physical or mental condition which existed before the policy issuance date or the policy effective date (whichever is the later) and which was not disclosed in the application;

(h) violation or attempted violation of the law or participation in fight or affray or resistance to arrest;

(i) war, whether declared or undeclared, revolution or any warlike operations;

(j) engaging in services in armed forces in times of declared or undeclared war or while under orders for warlike operations or restoration of public order;

(k) operating, being transported, or in any way engaging in air travel except as a fare paying passenger or cabin crew in any aircraft operated by a commercial passenger airline on a regular scheduled passenger trip over its established passenger route; and

(l) any congenital conditions.

Notes: “Cigna Healthcare”, “the Company”, “We”, “our” or “us” herein refer to Cigna Worldwide General Insurance Company Limited.

Contact Us

Connect with us

Individual Health Insurance

Group Health Insurance

Critical Illness Plan

Health & Wellness

About Us

Cigna Worldwide General Insurance Company Limited has been authorized and regulated by the Insurance Authority to carry out general insurance business in or from the Hong Kong SAR. Cigna Worldwide General Insurance Company Limited ("Cigna Healthcare"), © Cigna Healthcare. All rights reserved